Untuk mengarahkan perusahaan-perusahaan portofolionya menuju pertumbuhan, perusahaan-perusahaan Bentuk Usaha Tetap mengandalkan berbagai alat untuk bertahan dalam resesi global dan peralihan ke lingkungan pekerjaan jarak jauh. Mulai dari suntikan modal, bantuan proses restrukturisasi, hingga penerapan teknologi, perusahaan-perusahaan bekerja sama dengan perusahaan-perusahaan dalam portofolio mereka untuk mempertahankan relevansi pasar.

Tentu saja, perusahaan ekuitas swasta jarang berada dalam posisi yang lebih baik dari segi sumber daya untuk mendukung portofolio mereka. Preqin melaporkan Bentuk Usaha Tetap mencatat rekor US$1.46 triliun bubuk kering, yang sangat penting dalam menyusun strategi baru bagi perusahaan-perusahaan portofolio mereka untuk keluar dari pandemi dengan lebih kuat.

Selain itu, dibandingkan dengan krisis 2008 , pasar pinjaman swasta tiga kali lebih besar dan lebih matang, menurut perusahaan pengelola investasi Alvarium Investments. Pertumbuhan ini memungkinkannya untuk mengisi kekosongan yang ditinggalkan oleh bank-bank yang ragu-ragu melakukan investasi besar di tengah ketidakpastian yang dipicu oleh virus.

Berdasarkan Survei Pertengahan Tahun Bentuk Usaha Tetap S&P dalam skala global yang diterbitkan pada bulan September 2020, perusahaan Bentuk Usaha Tetap memperkirakan akan memfokuskan upaya mereka pada melakukan investasi baru yang selektif dan menstabilkan portofolio mereka saat ini sementara penggalangan dana tampaknya akan dikesampingkan untuk ke depannya. Bagaimana para investor ekuitas swasta melaksanakan upaya penyeimbangan ini, dan bagaimana strategi ini akan membantu portofolio mereka menjadi lebih tangguh terhadap perubahan pasar di masa depan?

Strategi ruang perang: Senjata Private Equity untuk mengatasi tantangan portofolio

Pandemi ini menimbulkan gangguan kesehatan dan bisnis yang besar, yang menuntut adanya penemuan kembali bisnis. Hal ini juga menciptakan hambatan besar terhadap pelaksanaan transaksi dan pergeseran valuasi bagi perusahaan Bentuk Usaha Tetap. Covid-19 juga mengungkap kelemahan model bisnis di dalam perusahaan-perusahaan portofolio mereka.

Dalam jangka menengah, pakar keuangan Natasha Ketabchi memperkirakan dana Bentuk Usaha Tetap akan melakukan salah satu dari tiga hal berikut:

- Lakukan penghematan di pasar lokal dan manfaatkan insentif kebijakan publik yang sudah ada untuk menghadapi badai.

- Memperdalam spesialisasi sektor mereka untuk menjadi spesialis di sektor-sektor yang berkembang pesat di tengah pandemi.

- Lakukan pergerakan strategis berdasarkan margin EBITDA yang dicapai melalui kombinasi penggunaan dana cadangan dan peningkatan fleksibilitas.

Dalam jangka panjang, Alvarium Investments mengantisipasi bahwa stabilitas dan ketahanan akan lebih diutamakan daripada pertumbuhan bagi perusahaan-perusahaan dalam portofolio Bentuk Usaha Tetap, dengan memprioritaskan pembangkitan arus kas daripada pengurasan arus kas.

Perusahaan Bentuk Usaha Tetap telah mendirikan “ruang perang tunai”

Cash war room bermanfaat bagi perusahaan yang menghadapi masalah likuiditas dan permintaan yang menurun. Mereka fokus pada tiga tugas tertentu:

- Mempercepat penilaian risiko dan mendeteksi potensi penghematan.

- Mengidentifikasi pengungkit uang tunai

- Berkolaborasi dengan para pemimpin bisnis dan pakar eksternal.

Ruang perang kas dapat beroperasi dari jarak jauh selama ia mempertahankan jalur komunikasi yang konstan antara CFO, bendahara, dan kelompok eksekutif perusahaan. Melalui alat bantu digital, dasbor terpusat yang menunjukkan neraca perusahaan dan diagnostik arus kas dapat dirancang dan diluncurkan secara real-time, untuk mempercepat pengambilan keputusan.

Tujuan utama dari war room adalah untuk mencapai kondisi operasional yang normal di tengah ketidakpastian. Perusahaan Bentuk Usaha Tetap perlu mencegah perusahaan portofolio mereka dari mengurangi investasi mereka selama penurunan ekonomi — sebuah pelajaran yang dipetik selama krisis keuangan tahun 2008. Mereka juga membantu perusahaan portofolio menyesuaikan penawaran produk dan layanan kepada klien mereka, mendesain ulang struktur kontrak untuk memperkuat loyalitas pelanggan, dan bersiap untuk merger dan akuisisi.

Menara pengontrol pengeluaran menjaga agar biaya tetap terkendali.

Meskipun ruang perang terutama berfungsi untuk menjaga likuiditas, perusahaan Bentuk Usaha Tetap juga menerapkan “ Menara Pengendalian Pengeluaran” (SCT) untuk mewujudkan komitmen perusahaan portofolio mereka dalam memberikan penghematan saat mereka menghadapi gelombang Covid-19 .

Biasanya dirancang untuk beroperasi dalam jangka waktu tetap antara enam hingga 12 bulan, SCT adalah badan pengambilan keputusan terpusat di mana kebutuhan pengeluaran diajukan oleh para manajer perusahaan. Hasilnya adalah proses tabungan yang lebih efisien. Meskipun SCT tidak mengelola biaya langsung penjualan barang, SCT mengawasi hampir semua hal lainnya, termasuk pembelian di titik penjualan, faktur, laporan pengeluaran, dan pengeluaran berulang.

Pendekatan ini bukannya tanpa tantangan karena jangkauannya lebih dari sekadar memodifikasi proses dan perilaku; SCT bahkan dapat mengubah pola pikir dan budaya seputar anggaran dan pengeluaran. Agar berhasil, tim SCT membutuhkan mandat dari atas ke bawah yang jelas serta keterlibatan penuh dari manajemen senior.

Perbedaan regional dalam respons portofolio Covid-19 perusahaan ekuitas swasta

Pasar Bentuk Usaha Tetap Eropa mengungguli negara-negara lain di dunia pada 2019. Dana LBO Benelux, Nordik, dan Inggris memberikan imbal hasil terkuat di antara negara-negara Eropa tahun lalu, dengan IRR masing-masing sebesar 16.64 persen, 16.29 persen, dan 15.6 persen.

Dana di negara-negara DACH-Jerman, Austria, dan Swiss-mengalami peningkatan kinerja yang tajam, dengan IRR sebesar 10.9 persen, naik dari 5.8 persen pada tahun sebelumnya.

Hal ini berlanjut hingga Juni 2020, dengan perusahaan Bentuk Usaha Tetap yang sebagian besar berasal dari Eropa menunjukkan semangat tinggi di benua tersebut, meskipun proyeksi pendapatan terdampak dan strategi keluar dihentikan sementara.

Melihat ke 2021, optimisme berlanjut — 74 persen dari perusahaan Bentuk Usaha Tetap yang disurvei menyatakan mereka siap berbisnis dan mencari peluang investasi baru dalam waktu dekat, dan 61 persen optimis untuk kembali berbisnis seperti biasa pada 2021.

Pada bulan September 2020, wilayah tersebut berada di jalur yang tepat untuk memberikan kinerja yang patut dipuji, meskipun tidak mencapai tingkat tahun lalu. Program bantuan publik untuk bisnis, yang dipadukan dengan tindakan cepat pemerintah untuk memberlakukan penguncian wilayah (lockdown) sejak dini, sangat berperan dalam pemulihan.

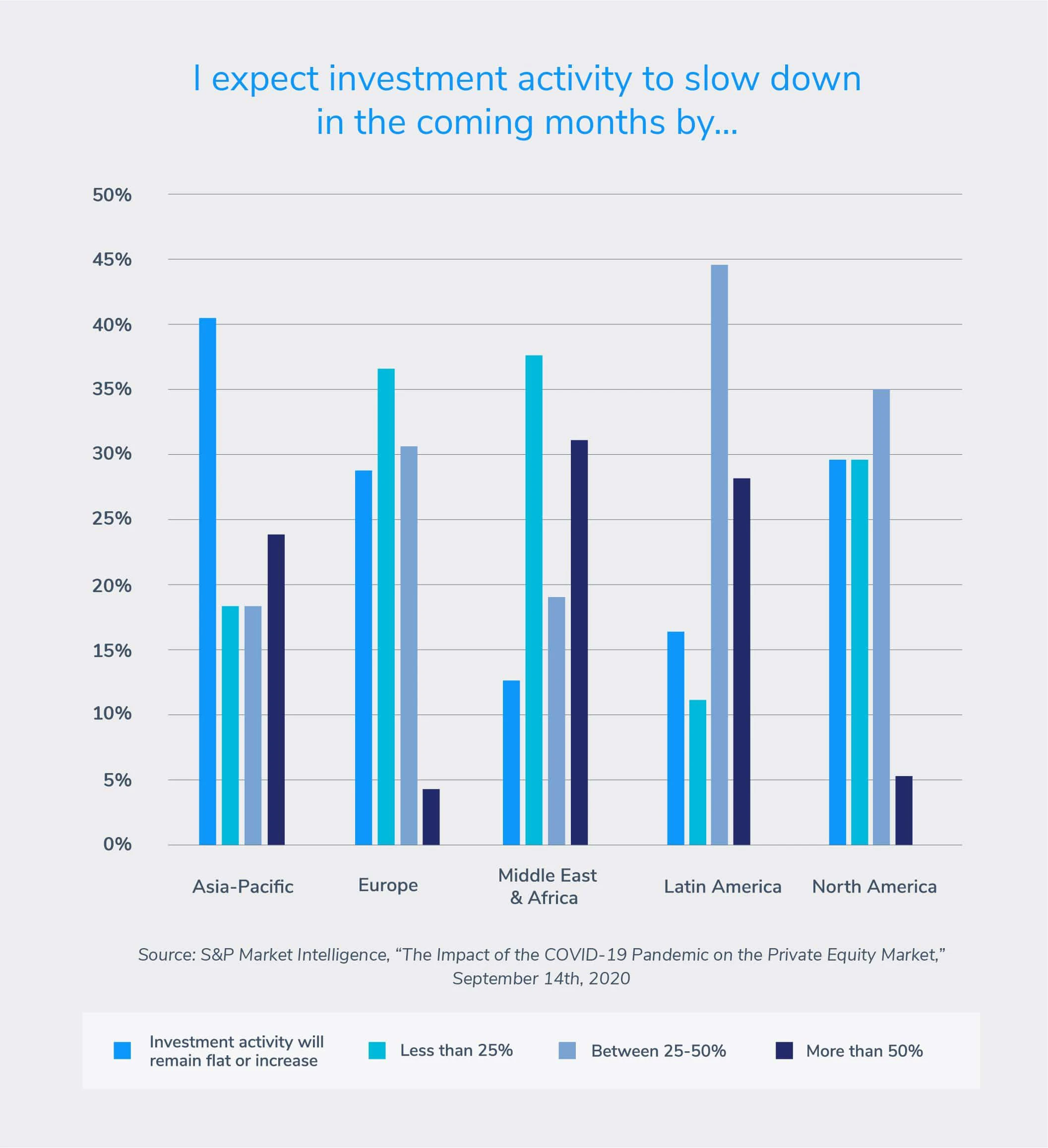

Investor Asia-Pasifik merupakan investor yang paling optimis di antara perusahaan Bentuk Usaha Tetap yang disurvei dalam Survei Bentuk Usaha Tetap Tengah Tahun S&P. Empat puluh persen mengantisipasi pandangan positif ketika mempertimbangkan lanskap pasca-Covid.

Optimisme ini mungkin berakar pada fakta bahwa Asia adalah yang pertama kali menghadapi virus ini, menjadikan kawasan ini sebagai pelopor dalam perjalanan menuju pemulihan, dengan menyaksikan sedikit peningkatan investasi.

Data S&P Global Market Intelligence menemukan bahwa nilai masuk Bentuk Usaha Tetap dan VC di kawasan APAC meningkat sebesar 31 persen, dari US$23.7 miliar pada 1Q20 menjadi US$31.2 miliar pada 2Q20.

22 persen responden yang mengantisipasi terhambatnya kegiatan investasi sebesar 50 persen mungkin terkait dengan kesulitan yang lazim terjadi di India dalam menangani pandemi.

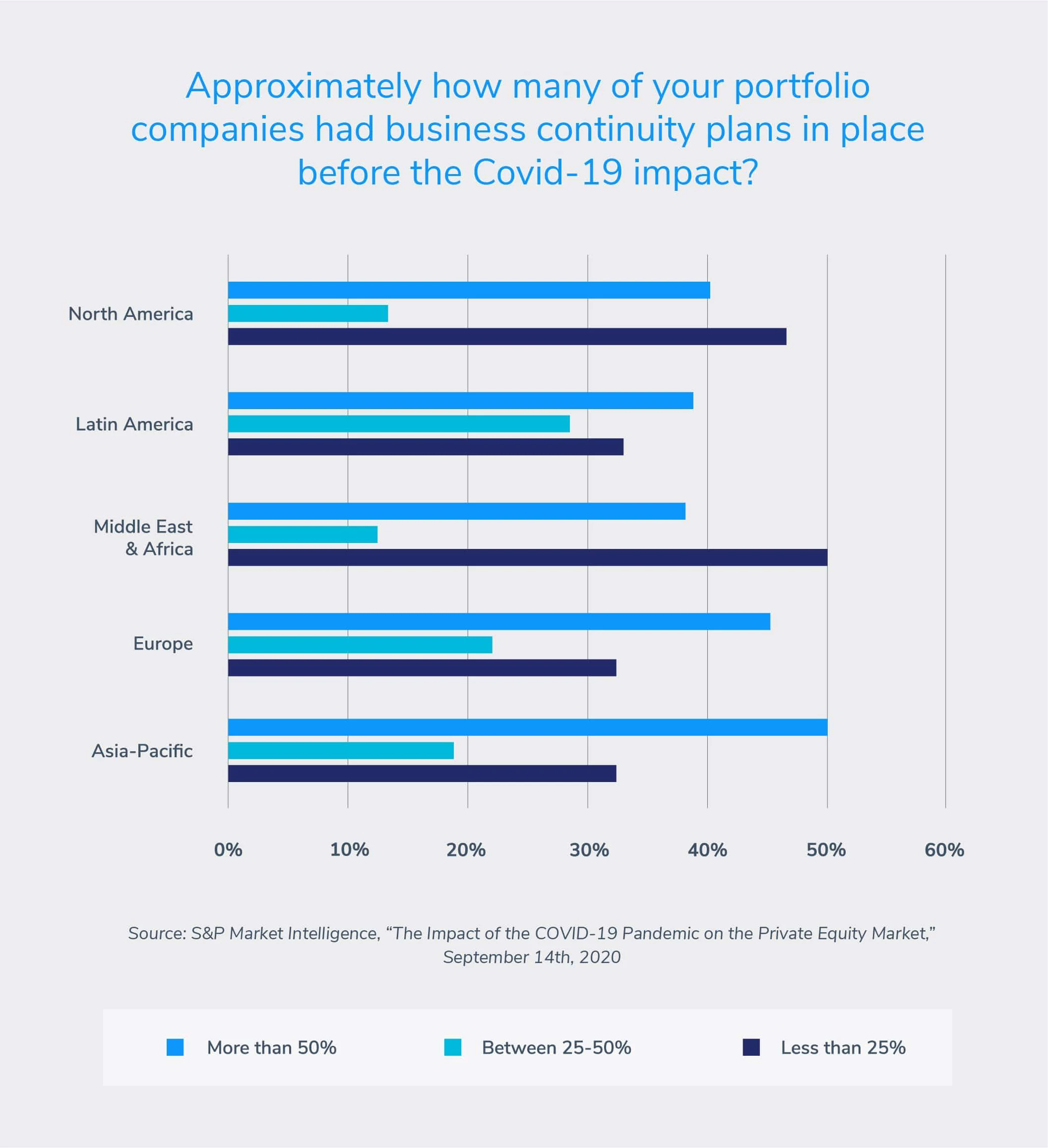

Perusahaan Bentuk Usaha Tetap harus memiliki rencana keberlanjutan bisnis yang telah ditetapkan untuk menjamin ketahanan di masa depan di seluruh perusahaan portofolio mereka. Survei S&P menemukan bahwa, rata-rata, 40 persen perusahaan yang disurvei mengisyaratkan lebih dari separuh perusahaan portofolio mereka memiliki rencana kelangsungan bisnis sebelum wabah Covid-19.

Responden Asia Pasifik melaporkan persentase tertinggi di 50 persen. Hal ini mungkin disebabkan oleh pengalaman wilayah ini sebelumnya dalam memerangi epidemi lokal.

Sebaliknya, perusahaan portofolio yang berbasis di Amerika Utara adalah yang paling tidak siap menghadapi gangguan bisnis yang parah. Empat puluh enam persen perusahaan Bentuk Usaha Tetap di Amerika Utara melaporkan bahwa kurang dari 25 persen portofolio mereka memiliki rencana kontingensi bisnis yang siap. Survei ini menekankan perlunya perancangan dan implementasi strategi bisnis yang kokoh untuk mencapai pertumbuhan, keberlanjutan, dan ketahanan.

Mendorong pertumbuhan strategis

Tambahkan nilai pada portofolio Anda - manfaatkan mitra yang tepat untuk membantu perusahaan portofolio agar berhasil, bahkan di masa ekonomi yang tidak menentu. Unduh panduan kami tentang mendorong pertumbuhan strategis untuk mempelajari lebih lanjut tentang bagaimana kami dapat membantu Anda.